Navigating the Best Student Loans: Your Guide to Smart Education Financing

Pursuing higher education is a transformative journey, but the rising cost of tuition often makes it a daunting financial challenge. With the average student loan debt in the U.S. exceeding $37,000 per borrower, selecting the best student loans isn’t just a choice. it’s a critical step toward securing your future without compromising your financial stability. Whether you’re an undergraduate, graduate student, or a parent planning for your child’s education, understanding your loan options can mean the difference between manageable repayments and decades of stress.

This comprehensive guide dives deep into the world of student loans, highlighting top options, key features, and strategies to optimize your borrowing experience. Let’s explore how to make informed decisions that align with your academic and financial goals.

Understanding Student Loans: Federal vs. Private

Before comparing lenders, it’s essential to grasp the two primary categories of student loans: federal loans (government-backed) and private loans (offered by banks, credit unions, and online lenders). Each has distinct advantages and drawbacks, depending on your circumstances.

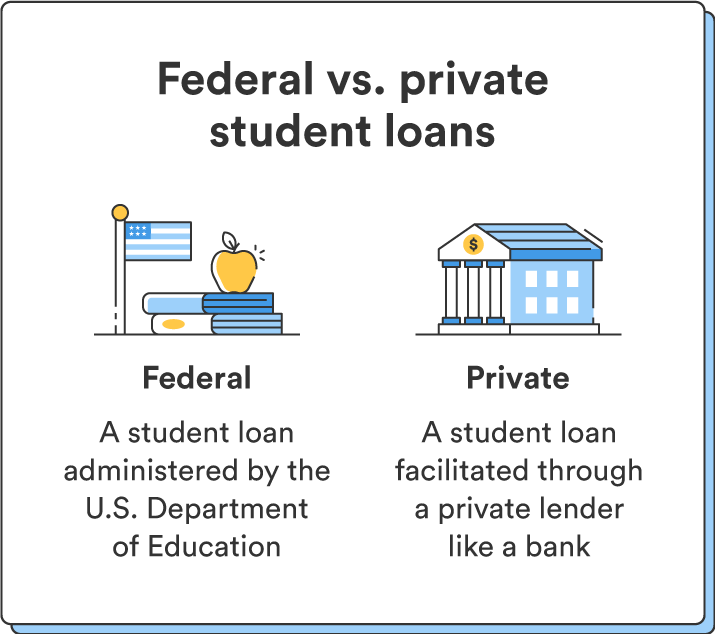

Federal Student Loans

Administered by the U.S. Department of Education, federal loans are widely regarded as the first stop for students due to their borrower-friendly terms:

- Fixed Interest Rates: Rates are set by Congress and typically lower than private loans (e.g., 5.50% for undergraduates in 2024).

- Income-Driven Repayment (IDR) Plans: Payments adjust based on income, with forgiveness after 20–25 years.

- Loan Forgiveness Programs: Public Service Loan Forgiveness (PSLF) discharges remaining debt after 10 years of qualifying payments for nonprofit/government employees.

- Deferment and Forbearance: Options to pause payments during financial hardship.

- Subsidized Loans: The government covers interest while you’re in school (for eligible undergraduates with financial need).

Best For: Students seeking flexibility, lower rates, and forgiveness options.

Private Student Loans

Private lenders like Sallie Mae, Discover, and SoFi offer loans that fill gaps when federal aid falls short. Key features include:

- Higher Borrowing Limits: Cover up to 100% of attendance costs.

- Variable or Fixed Rates: Competitive rates for creditworthy borrowers (as low as 3.5% APR).

- Customizable Terms: Repayment periods from 5 to 20 years.

- Cosigner Release: Remove a cosigner after meeting credit criteria.

Best For: Borrowers with strong credit (or a cosigner) needing additional funds beyond federal limits.

Features of the Best Student Loans

When evaluating the best student loans, prioritize these features to minimize long-term costs and maximize flexibility:

1. Competitive Interest Rates

- Federal Loans: Fixed rates (no credit check required).

- Private Loans: Rates vary by credit profile. A 1% difference can save thousands over time.

2. Flexible Repayment Options

- In-School Deferment: Postpone payments until after graduation.

- Grace Periods: 6–9 months post-graduation before repayment starts.

- IDR Plans: Cap payments at 10–20% of discretionary income (federal only).

3. Low or No Fees

Avoid loans with origination fees (e.g., federal loans charge 1.057% fees). Many private lenders have eliminated these costs.

4. Cosigner Support

Students without credit histories can qualify for better rates by adding a creditworthy cosigner.

5. Loan Forgiveness and Discharge Options

Federal loans offer unique protections, including disability discharge, closed school discharge, and death benefits.

Benefits of Choosing the Best Student Loans

Selecting the right loan unlocks long-term advantages:

- Lower Total Debt: Competitive rates and fees reduce lifetime interest.

- Stress-Free Repayment: Align payments with post-graduation income.

- Credit Building: Consistent payments improve credit scores.

- Focus on Education: Avoid financial distractions during school.

Use Cases: Which Loan is Right for You?

Scenario 1: The Undergraduate with Financial Need

Recommended: Federal Subsidized Loans.

- Pros: No interest accrual during school; fixed rates.

Scenario 2: The Graduate Student Pursuing Medicine/Law

Recommended: Federal Grad PLUS Loans.

- Pros: High borrowing limits; access to PSLF.

Scenario 3: The Borrower with Excellent Credit

Recommended: Private Student Loans.

- Pros: Lower rates than federal options; quick approval.

Scenario 4: Refinancing Post-Graduation

Recommended: Private Refinancing Lenders (e.g., Earnest, Laurel Road).

- Pros: Lower rates; single monthly payment.

How to Choose the Best Student Loan

- Exhaust Federal Options First: Complete the FAFSA to unlock grants, work-study, and federal loans.

- Compare Private Lenders: Use tools like Credible or NerdWallet to prequalify without hurting your credit.

- Calculate Total Costs: Factor in interest, fees, and repayment timelines.

- Read Reviews: Check BBB ratings and customer feedback on servicer responsiveness.

- Consult a Financial Advisor: Tailor choices to your career trajectory and earning potential.

Call to Action: Secure Your Future Today

Don’t let confusion or procrastination derail your educational dreams. Start by:

- Submitting Your FAFSA: Visit StudentAid.gov to apply for federal aid.

- Prequalifying with Private Lenders: Compare rates in minutes at Credible.

- Exploring Forgiveness Programs: Bookmark the PSLF Help Tool if pursuing public service.

Your education is an investment—finance it wisely.

FAQ: Addressing Common Student Loan Questions

Q1: Should I choose federal or private student loans?

A: Federal loans are ideal for most borrowers due to flexible repayment and forgiveness. Use private loans only after maxing federal aid.

Q2: Do I need a cosigner for private student loans?

A: Often yes, unless you have strong credit (e.g., 670+ FICO score and steady income).

Q3: Can I refinance federal loans?

A: Yes, but you’ll lose federal benefits like IDR and PSLF. Refinance only if saving on interest outweighs these perks.

Q4: How does interest capitalization work?

A: Unpaid interest is added to the principal balance after deferment/grace periods, increasing total debt. Prioritize paying interest early.

Q5: What if I can’t afford my payments?

A: Federal borrowers can switch to IDR plans. Private borrowers may request forbearance or refinance.

Q6: Are there loans for international students?

A: Yes, but they typically require a U.S. cosigner. Explore lenders like Prodigy Finance or MPower.

Q7: How long does loan approval take?

A: Federal loans process via FAFSA in 3–5 days. Private loans can approve within minutes and disburse in weeks.

Final Thoughts

Choosing the best student loans requires balancing immediate needs with long-term financial health. By prioritizing federal aid, shopping around for private lenders, and understanding repayment strategies, you can invest in your education without sacrificing your future. Start your journey today—your smarter, debt-free self will thank you.